With the end of the financial year 2025-26 on March 31, 2026, the manufacturing firms in India are confronting a critical period in closing books, compliance, and having rightful financial statements. The manufacturing industry has its own set of complexities, like inventory valuation, fixed asset management, production costing, supply chain reconciliations, and industry-specific regulations under the GST, Income Tax, Companies Act, and environmental regulations.

An effectively performed year-end process reduces audit risks, maximizes the tax position, contributes to the correct reporting under Ind AS (notable companies use the approach), and prepares a solid base for FY 2026-27.

This multi-purpose checklist addresses the most vital areas of focus that are specific to the manufacturers based on best practices in inventory management, financial reconciliations, statutory compliance, and new regulatory changes.

Inventory Management and Valuation

Inventory often represents a significant portion of a manufacturer's assets, making an accurate year-end assessment essential for the correct cost of goods sold (COGS), gross margins, and balance sheet integrity.

- Conduct a physical inventory count of raw materials, work-in-progress (WIP), semi-finished goods, and finished goods. Use cycle counting where possible throughout the year to reduce year-end burden, but perform a full or representative physical verification near March 31.

- Reconcile physical counts with perpetual inventory records in your ERP system. Investigate and adjust for discrepancies (shrinkage, obsolescence, damage, or theft).

- Value inventory using consistent methods (e.g., FIFO, weighted average, or standard costing) as per applicable accounting standards. Assess net realizable value (NRV) and make provisions for slow-moving or obsolete stock.

- Review cutoff procedures for goods in transit, receipts, and dispatches around March 31 to ensure proper period allocation.

- Update inventory policies and document any changes for audit trails.

Tip for Manufacturers: Coordinate with production teams to minimize disruptions—schedule counts during low-production periods or plant shutdowns if feasible.

Also Read: Govt Cuts Excise Duty on Petrol and Diesel: What It Means for You?

Financial Reconciliations and Account Closures

Ensure all transactions are captured accurately before finalizing the trial balance.

- Reconcile bank accounts, credit cards, loans, and cash balances with statements.

- Verify accounts receivable (debtors confirmation, aging analysis, provisions for doubtful debts) and accounts payable (creditor confirmations, clearing unmatched invoices).

- Review and post adjusting entries for accruals, prepayments, depreciation, amortization, and provisions (e.g., warranties, returns, or environmental liabilities common in manufacturing).

- Reconcile intercompany transactions, fixed assets (including additions, disposals, and impairment tests), and GST Input Tax Credit (ITC) ledgers.

- Generate key financial statements: Balance Sheet, Profit & Loss, Cash Flow Statement, and supporting schedules. Analyze variances in margins, working capital, and production costs.

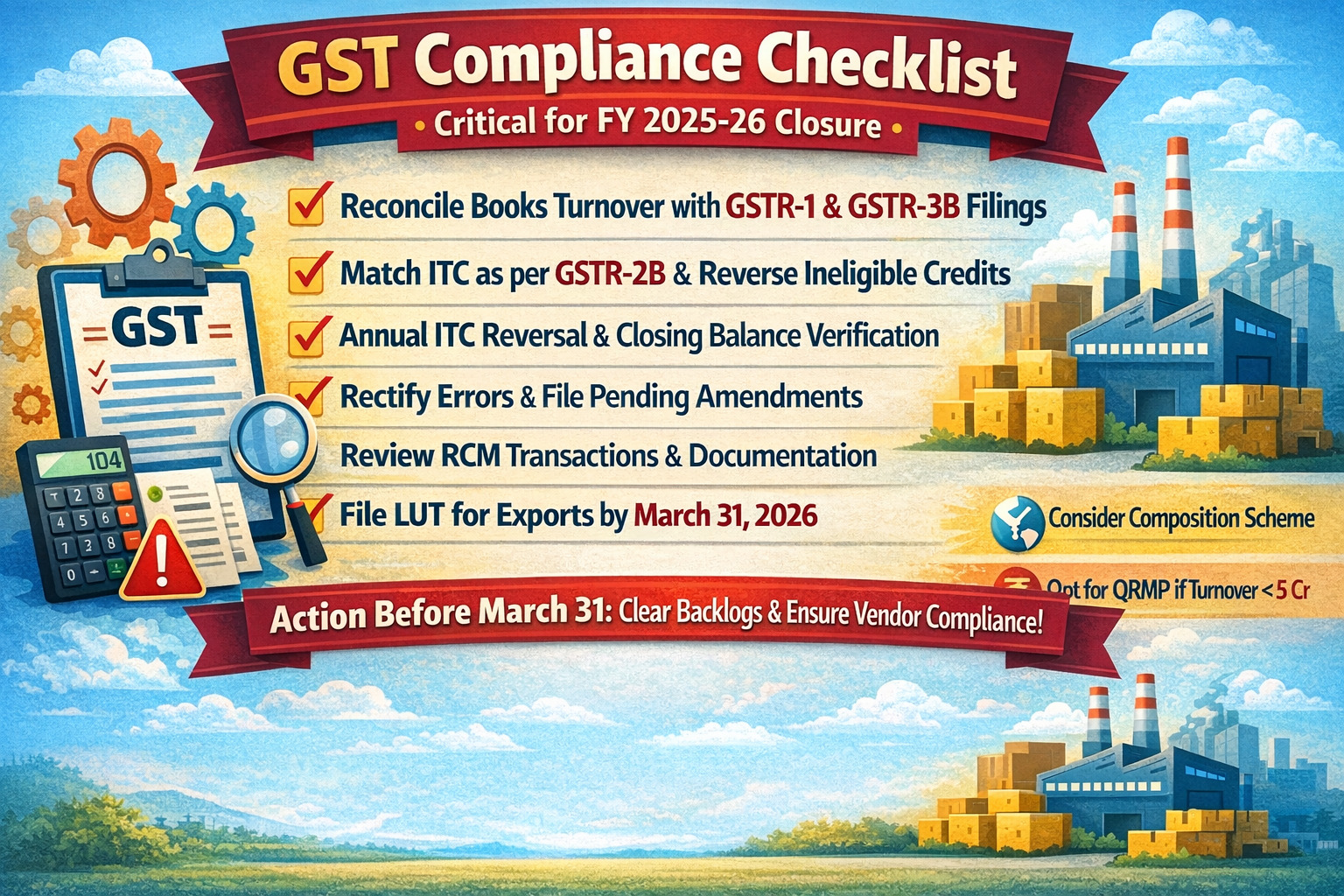

GST Compliance Checklist (Critical for FY 2025-26 Closure)

Manufacturing units deal with high-volume inward/outward supplies, making GST reconciliations vital to avoid ITC disallowances or penalties.

- Reconcile books turnover with GSTR-1 and GSTR-3B filings (including credit/debit notes).

- Match ITC as per GSTR-2B with purchase registers; claim eligible credits and reverse ineligible ones (e.g., under Rule 42/43 for exempt supplies or capital goods).

- Perform annual ITC reversal calculations and ensure closing ITC balances match between books and the GST portal.

- File any pending amendments or rectify errors in prior returns (where allowed).

- Review Reverse Charge Mechanism (RCM) transactions and documentation.

- File Letter of Undertaking (LUT) for zero-rated exports (for FY 2026-27) by March 31, 2026, if applicable. Consider opting for the Composition Scheme or QRMP (if turnover < ₹5 Cr) by the relevant deadlines.

Action Before March 31: Clear any backlog in returns and ensure vendor compliance for seamless ITC flow.

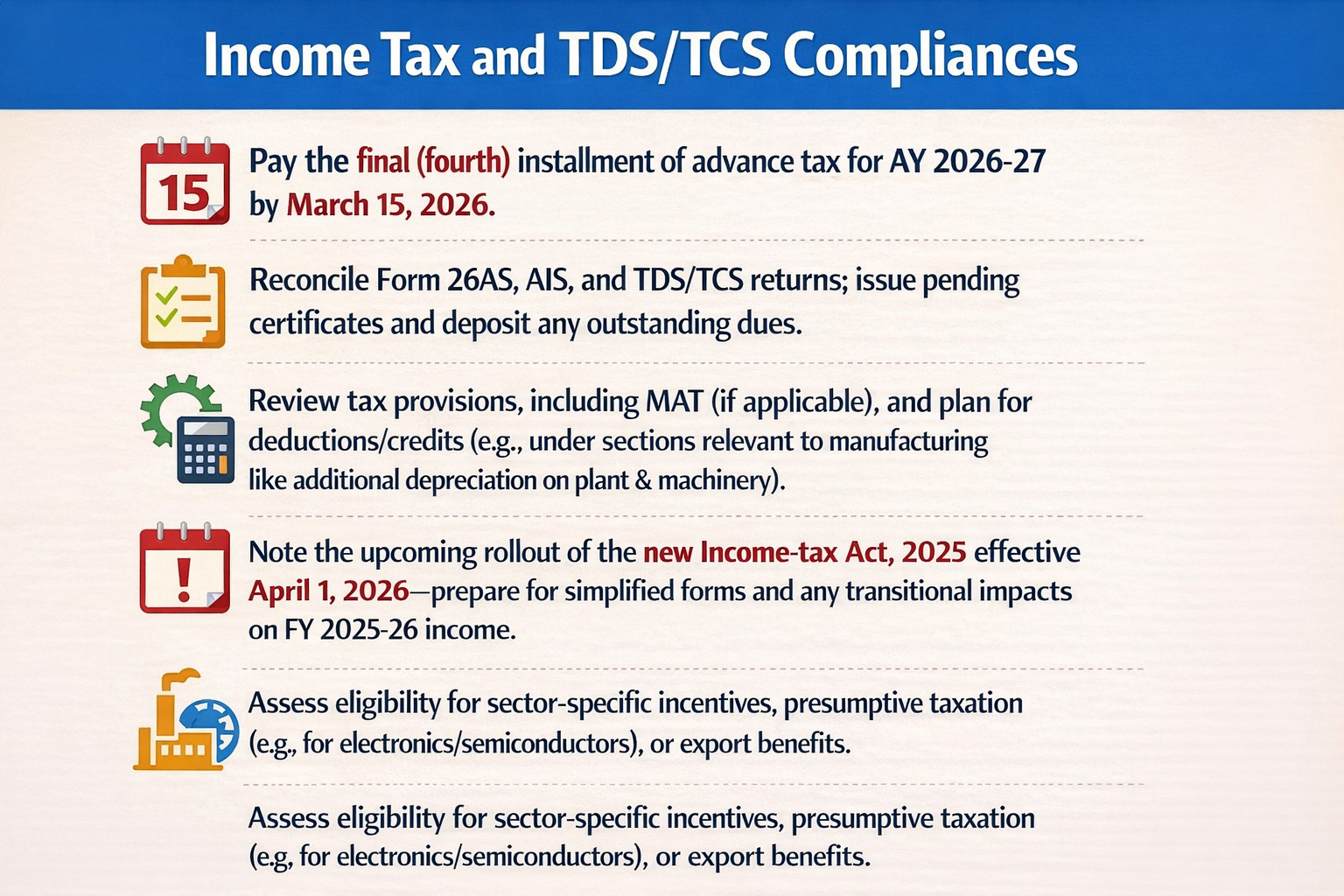

Income Tax and TDS/TCS Compliances

- Pay the final (fourth) installment of advance tax for AY 2026-27 by March 15, 2026.

- Reconcile Form 26AS, AIS, and TDS/TCS returns; issue pending certificates and deposit any outstanding dues.

- Review tax provisions, including MAT (if applicable), and plan for deductions/credits (e.g., under sections relevant to manufacturing like additional depreciation on plant & machinery).

- Note the upcoming rollout of the new Income-tax Act, 2025 effective April 1, 2026—prepare for simplified forms and any transitional impacts on FY 2025-26 income.

- Assess eligibility for sector-specific incentives, presumptive taxation (e.g., for electronics/semiconductors), or export benefits.

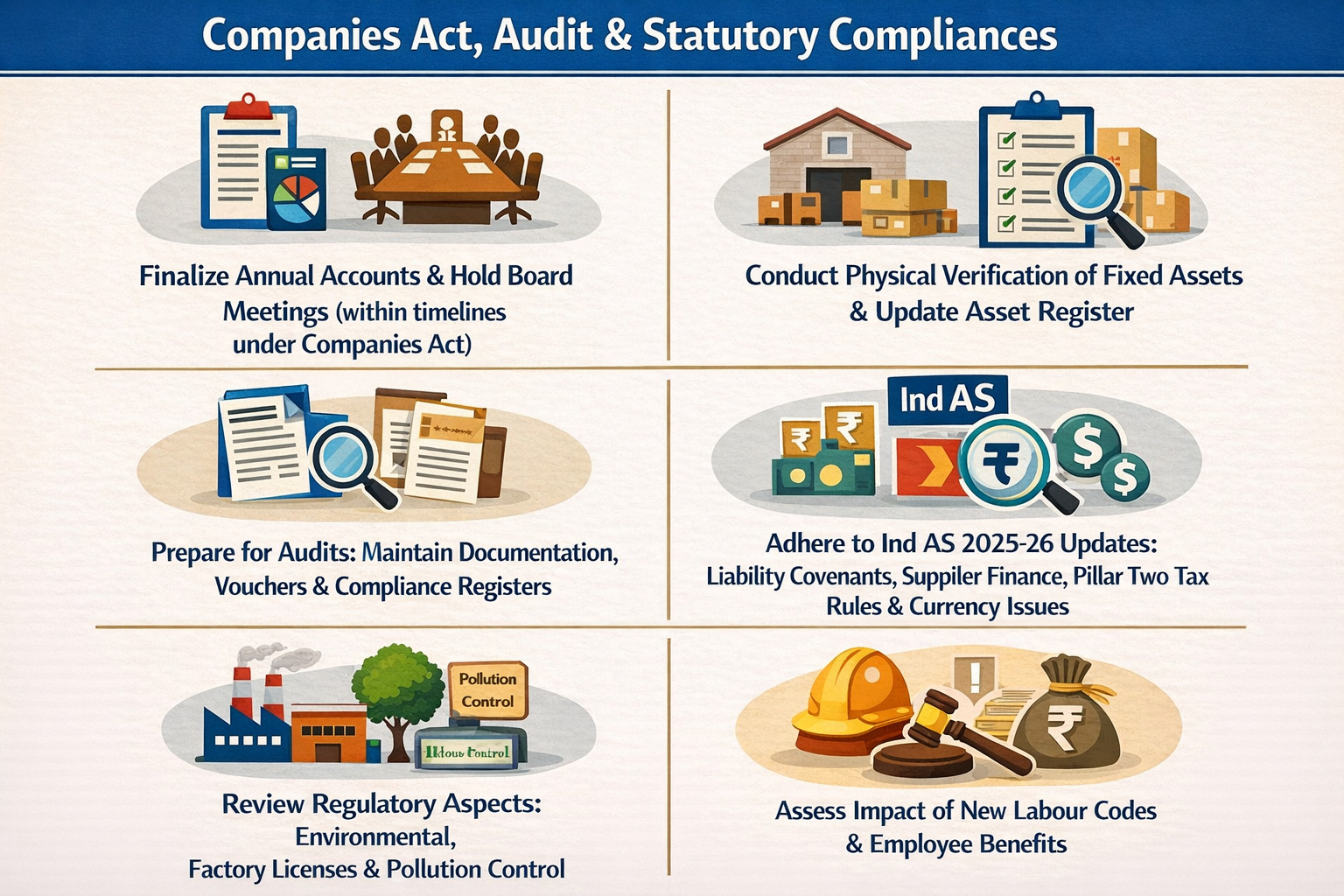

Companies Act, Audit, and Statutory Compliances

- Finalize annual accounts and hold board meetings to adopt them (within timelines under Companies Act).

- Conduct physical verification of fixed assets and update the asset register.

- Prepare for statutory/internal audits: Maintain proper documentation, vouchers, contracts, and compliance registers.

- Ensure adherence to Ind AS amendments effective for FY 2025-26, including updated guidance on liability classification (covenants), supplier finance disclosures (Ind AS 7 & 107), Pillar Two global minimum tax exceptions (Ind AS 12), and foreign currency exchangeability. Also consider impacts from new Labour Codes on employee benefits and gratuity.

- Review other regulatory aspects: Environmental clearances, factory licenses, pollution control compliances, and any state-specific manufacturing incentives.

Payroll, HR, and Employee-Related Closures

- Finalize payroll for March, including variable pay, incentives, and deductions.

- Reconcile PF, ESI, professional tax, and labour welfare contributions.

- Issue Form 16 to employees and file relevant TDS returns.

- Update employee benefit obligations considering any changes from Labour Codes.

Operational and Forward-Looking Activities

- Review production costing, overhead absorption, and variance analysis for insights into efficiency.

- Assess working capital, cash flow trends, and budget vs. actuals for FY 2025-26.

- Identify cost-saving opportunities (e.g., supplier negotiations, inventory optimization) and prepare budgets/forecasts for FY 2026-27.

- Update risk registers, insurance policies, and contingency plans.

- Document all processes for smoother transitions and audit readiness.

Also Read: West Asia Crisis: Impact on Indian Exports Market

Best Practices for a Smooth Year-End Close

- Start early (ideally in January/February) with a detailed close calendar and assign responsibilities across finance, operations, procurement, and IT teams.

- Leverage ERP systems for real-time reconciliations and automated reports.

- Engage auditors or consultants in advance for manufacturing-specific issues like inventory observation.

- Maintain robust documentation to support any regulatory scrutiny.

- Use the process as an opportunity for continuous improvement—analyze trends in raw material costs, supply chain disruptions, or energy usage.

With the Financial Year 2025-26 ending on March 31, 2026, the year-end close should be considered a strategic necessity and not a legal obligation by manufacturing companies. Comprehensive implementation of the checklist, including accurate valuation of inventory, GST reconciliations, fixed asset validation, tax provisions, and Ind AS compliance, will mean that books are accurate, that audit risk is minimal as well as that the checklist provides useful information about costs, margins and operational efficiency.

This closure is the most appropriate opportunity to prepare to transition as the Income-tax Act, 2025, will come into effect on April 1, 2026, and introduce simplified provisions, streamlined compliances, and further incentives to new manufacturing units. Discipline is effective in enhancing financial integrity, maximizing tax positions, and enhancing resilience in a competitive industry with the help of Make in India and PLI schemes.